The literature in portfolio optimisation has been around for decades. In this post I cover a number of traditional portfolio optimisation models. The general aim is to select a portfolio of assets out of a set of all possible portfolios being considered with a defined objective function.

The data:

The data is collected using the tidyquant() package’s tq_get() function. I then convert the daily asset prices to daily log returns using the periodReturn function from the quantmod() package. Next I construct lists of 6 months worth of daily returns using the rolling_origin() function from the rsample() package. The objective is to compute on a rolling basis the 6 month mean returns mus and the 6 month covariance matrices Sigmas on the training sets (i.e. 6 months) and apply them on the test sets (i.e. 1 month later) – monthly rebalancing.

Just as with the returns data, the same is applied to the monthly prices data.

The returns data for the first split looks like the following:

AAPL

ABBV

A

APD

AA

CF

NVDA

HOG

WMT

AMZN

0.000000000

0.000000000

0.000000000

0.0000000000

0.000000000

0.000000000

0.0000000000

0.000000000

0.0000000000

0.0000000000

-0.012702708

-0.008291331

0.003575412

-0.0035002417

0.008859253

-0.004740037

0.0007860485

-0.020819530

-0.0063746748

0.0045367882

-0.028249939

-0.012713395

0.019555411

0.0133515376

0.020731797

0.022152033

0.0324601827

-0.005529864

0.0037720098

0.0025886574

-0.005899428

0.002033327

-0.007259372

-0.0009230752

-0.017429792

-0.003753345

-0.0293228286

0.006958715

-0.0096029606

0.0352948721

0.002687379

-0.022004791

-0.008022622

0.0018451781

0.000000000

-0.014769161

-0.0221704307

-0.003063936

0.0027737202

-0.0077780140

-0.015752246

0.005620792

0.026649604

0.0133906716

-0.002200109

0.034376623

-0.0226730363

0.038724890

-0.0002916231

-0.0001126237

The statistics

The Mus (mean returns) data looks like:

x

AAPL

-0.0025241

ABBV

0.0014847

A

0.0002314

APD

0.0006546

AA

-0.0010700

CF

-0.0013681

NVDA

0.0008864

HOG

0.0008061

WMT

0.0006895

AMZN

0.0006147

The Sigmas (covariance matrix) data looks like:

AAPL

ABBV

A

APD

AA

CF

NVDA

HOG

WMT

AMZN

AAPL

0.0004166

0.0000220

0.0000112

0.0000388

0.0000528

0.0000277

0.0000408

0.0000116

-0.0000038

-0.0000366

ABBV

0.0000220

0.0003128

0.0000490

0.0000393

0.0000137

0.0000472

0.0000511

0.0000732

0.0000258

0.0000295

A

0.0000112

0.0000490

0.0002061

0.0000720

0.0000741

0.0000885

0.0000930

0.0001175

0.0000371

0.0001139

APD

0.0000388

0.0000393

0.0000720

0.0000993

0.0000523

0.0000687

0.0000578

0.0000744

0.0000107

0.0000511

AA

0.0000528

0.0000137

0.0000741

0.0000523

0.0001485

0.0000874

0.0000685

0.0000674

-0.0000012

0.0000383

CF

0.0000277

0.0000472

0.0000885

0.0000687

0.0000874

0.0002271

0.0000706

0.0000900

-0.0000112

0.0000606

NVDA

0.0000408

0.0000511

0.0000930

0.0000578

0.0000685

0.0000706

0.0002092

0.0000706

0.0000127

0.0000853

HOG

0.0000116

0.0000732

0.0001175

0.0000744

0.0000674

0.0000900

0.0000706

0.0002393

0.0000214

0.0000895

WMT

-0.0000038

0.0000258

0.0000371

0.0000107

-0.0000012

-0.0000112

0.0000127

0.0000214

0.0000682

0.0000236

AMZN

-0.0000366

0.0000295

0.0001139

0.0000511

0.0000383

0.0000606

0.0000853

0.0000895

0.0000236

0.0003118

Comparing Portfolio Optimisation

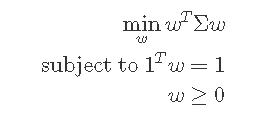

Global Minimum Variance Portfolio

The global minimum-variance portfolio is a portfolio of assets with gives us the lowest possible return variance or portfolio volatility. Volatility here is used as a replacement for risk, thus with less variance in volatility correlates to less risk in an asset. The portfolio focuses only on risk and ignores expected returns.

The objective function is;

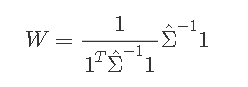

Since is unknown we can estimate it as with the covariance matrix. In which the convex solution becomes:

The objective is that we want to find the optimial weights from the model such that our risk is minimised.

The below problem consists of our problem . The quad_form function takes the quadratic form where is a vector and is a matrix or in our case ww is our weights vector and is the covariance matrix for . The constraints correspond to in which we cannot assign negative weights to our assets and that we invest all our capital in the portfolio.

We can use the Disciplined Convex Programming (CVXR) package in R, which;

Analyses the problem,

Verifies the convexity,

Converts the problem into canonical form,

Solves the problem.

We want to find the optimial weights from the model such that our risk is minimised. We can do this by solving the optimisation problem, bind the lists into a single data frame and use ggplot2 to plot the rolling one month out of sample optimal portfolio weights – based on the previous 6 months rolled mus and Sigmas.

# 1) Function: Global Minimum Variance Portfolio

GMVPportolioFunction <- function(Sigma) {

w <- Variable(nrow(Sigma))

problem <- Problem( # Initialise the problem

Minimize( # minimse or maximise objective function

quad_form(

w, Sigma # Model inputs, the number of weights to consider and the covariance matrix

)

),

constraints = list(

w >= 0, # First model constraint

sum(w) == 1)) # Second model constrain

Solution <- solve(problem, solver="SCS") # Solves the problem

return(as.vector(Solution$getValue(w)))

}

# 1a) Portfolio GMVP

GMVPPortfolio <- map(

.x = Sigmas,

GMVPportolioFunction)

# 1b) Portfolio GMVP

GMVPPortfolioWeights <- setNames(GMVPPortfolio, ListNamesDates) %>%

map(., ~setNames(., c(symbols))) %>%

map_dfr(., ~bind_rows(.), .id = "date") %>%

mutate(date = as.Date(paste(date, "01"), format = "%Y %b %d"))

GMVPPortfolioWeights %>%

head() %>%

kable() %>%

kable_styling(bootstrap_options = c("striped", "hover", "condensed", "responsive"))

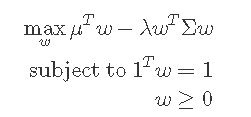

The Markowitz Mean-Variance Portfolio is constructed as follows:

We can set different risk parameters by adjusting and see how the returns are affected. This can be done by running multiple optimisation problems on the data with different values. Higher values places emphasis on the right hand side of the equation and thus the more risk adverse the investor is.

We can see how the risk and return is affected by the changes in the values in the following plot. As the values increase the less risk we take on but also we assume less returns. Low values of makes us invest in a signle asset with the weight on asset , increasing the values increases the weights in other assets spreading our risk.

Note: I originally made this post a few months back and when I went back to it some of the parts for the Max-Sharpe Ratio portfolio did not work as before – I think this is due to the recent update in the tidyr package. I made some minor adjustments, however this part of the post is incorrect (just look at the portfolio weights plot). I hightlight in the code when I made the minor adjustments – when I have the opportunity to go back through the code more carefully I will –

# 2) Function: Max Sharpe Ratio

#NOTE::: When we have all negative mus for a given month we obtain an NA value - the function

# cannot find a maximum when all mus are negative compare the MaxSharpePortfolio$`2015 Sep` and

# MaxSharpePortfolio$`2015 Oct` along with the mus$`2015 Sep` and mus$`2015 Oct` we invests 99% of the portfolio

# in Sept in ABBV since its positive. In Oct ABBV mu is negative and we cannot invest at all.

# Increasing the universe of Assets may overcome this problem.

MaxSharpeportolioFunction <- function(mu, Sigma) {

w <- Variable(nrow(Sigma))

problem <- Problem(

Minimize(quad_form(w, Sigma)),

constraints = list(

w >= 0, t(mu) %*% w == 1)

)

Solution <- solve(problem, solver="SCS")

return(as.vector(Solution$getValue(w)/sum(Solution$getValue(w))))

}

# 3a) Portfolio Max Sharpe Ratio

MaxSharpePortfolio <- purrr::map2(.x = mus,

.y = Sigmas,

.f = ~MaxSharpeportolioFunction(.x, .y))

# 3b) Portfolio Max Sharpe Ratio

MaxSharpePortfolioWeights <- setNames(MaxSharpePortfolio, ListNamesDates) %>%

as_tibble(.) %>% # Made an adjustment here

map(., ~setNames(., c(symbols))) %>%

map_dfr(., ~bind_rows(.), .id = "date") %>%

mutate(date = as.Date(paste(date, "01"), format = "%Y %b %d"))

MaxSharpePortfolioWeights %>%

head() %>%

kable() %>%

kable_styling(bootstrap_options = c("striped", "hover", "condensed", "responsive"))

date

AAPL

ABBV

A

APD

AA

CF

NVDA

HOG

WMT

AMZN

2013-07-01

0.0009088

0.1532283

0.0371040

0.2332344

-0.1010233

0.0126946

0.2083815

-0.0262255

0.5086221

-0.0269248

2013-08-01

0.0109744

0.1485344

-0.0156878

0.3292178

-0.0080488

0.0051372

0.1146053

0.0091278

0.4086911

-0.0025515

2013-09-01

0.1217206

0.1246626

0.0087004

0.3421645

0.0000000

0.0000000

0.2414533

0.0002820

0.1610166

0.0000000

2013-10-01

0.0270424

0.0000000

0.2268394

0.3427932

0.0000000

0.0000000

0.2653166

0.1283026

0.0000000

0.0097059

2013-11-01

0.2061379

0.0000000

0.1890218

0.2234739

0.0000000

0.0533254

0.0000000

0.0000000

0.0000000

0.3280410

2013-12-01

0.2252115

0.0000000

0.0306323

0.0724210

0.0000000

0.0325004

0.0000000

0.1907158

0.1192395

0.3292796

# 3c) Portfolio Max Sharpe Ratio

MaxSharpePortfolioWeights %>%

select(date, everything()) %>% # Made an adjustment here

pivot_longer(cols = 2:ncol(.), values_to = "weights") %>%

ggplot(aes(fill = name, y = weights, x = date)) +

geom_bar(position = "stack", stat = "identity", width = 100) +

scale_fill_viridis(option = "magma", discrete = TRUE, name = "Asset") +

theme_bw() +

ggtitle("Maximum Sharpe Ratio Rolling Portfolio Adjustments") +

xlab("Date") +

ylab("Weights")

Looking at the plots the Global Minimum Variance Portfolio shows the lowest volatility in the portfolio returns. The Max Sharpe portfolio is clearly wrong here (see, previous point on Max Sharpe Ratio section). The annaulised performance metrics are also displayed at the bottom for each portfolio over the period.

Plotting the cumulative returns shows that the Markowitz lambda portfolios have the highest returns over the period, however they also have the highest standard deviation over the same period.

chart.CumReturns(AllReturns, main = "Weighted Returns by Objective Function and Risk Tolerance",

wealth.index = TRUE, legend.loc = "topleft", colorset = rich6equal)

charts.PerformanceSummary(AllReturns, main = "Performance for Different Weighted Assets",

wealth.index = TRUE, colorset = rich6equal)

Additional

(Some additional test data I leave here for future reference)

is a portfolio of assets with gives us the lowest possible return variance or portfolio volatility. Volatility here is used as a replacement for risk, thus with less variance in volatility correlates to less risk in an asset. The portfolio focuses only on risk and ignores expected returns.

is a portfolio of assets with gives us the lowest possible return variance or portfolio volatility. Volatility here is used as a replacement for risk, thus with less variance in volatility correlates to less risk in an asset. The portfolio focuses only on risk and ignores expected returns.

is unknown we can estimate it as

is unknown we can estimate it as  with the covariance matrix. In which the convex solution becomes:

with the covariance matrix. In which the convex solution becomes:

problem

problem  . The

. The  where

where  is a vector and

is a vector and  is a matrix or in our case ww is our weights vector and

is a matrix or in our case ww is our weights vector and  . The

. The  in which we cannot assign negative weights to our assets and that we invest all our capital in the portfolio.

in which we cannot assign negative weights to our assets and that we invest all our capital in the portfolio.

and see how the returns are affected. This can be done by running multiple optimisation problems on the data with different

and see how the returns are affected. This can be done by running multiple optimisation problems on the data with different  , increasing the

, increasing the  spreading our risk.

spreading our risk.